Should You Rush Into a Variable Rate Mortgage?

Variable Rate Mortgages are much worse than they were 2 weeks ago. Regardless, if you or someone you know is in a fixed rate mortgage with a rate greater than 3% it might still be time to consider switching to a variable rate.

Why?

- The Prime Rate is as low as it has ever been.

- When fixed mortgage rates drop it will become more expensive for you to break your fixed rate mortgage.

So, why are the Banks inflating mortgage rates?

The Bank of Canada is buying $150 Billion dollars worth of mortgages from the Canadian Banks. Backstopping them against any losses. However, the banks have increased mortgage rates for Canadians citing increased risk. What risks are the banks taking on if their mortgages are guaranteed by the government? To quantify just how much profit this will add to the banks’ bottom line consider the following:

- The average mortgage in Toronto is about $275,000

- The Bank’s average increase in rate premium in the past 14 days regardless of fixed or variable rate is about 1% to 1.5%. This is in addition to the usual 1.20% to 1.50% spread they already take (this is explained below after the article) making the total premium Canadians are paying up to 3% in some cases.

This means for each Canadian mortgage, the banks are earning an additional $2,750 to $4,125 annually.

Want to Know More About the Spreads The Banks Earn?

Banks typically earn a spread on Canadian mortgages both variable and fixed that is 1.20% to 1.5%. For fixed rate mortgages, this is the difference between the government of Canada bond yield and the 5 year fixed rate mortgage. The Banks use the spread they earn to cover the cost to service the mortgage, meaning collecting payments and handing payouts, this is typically about 0.15%.

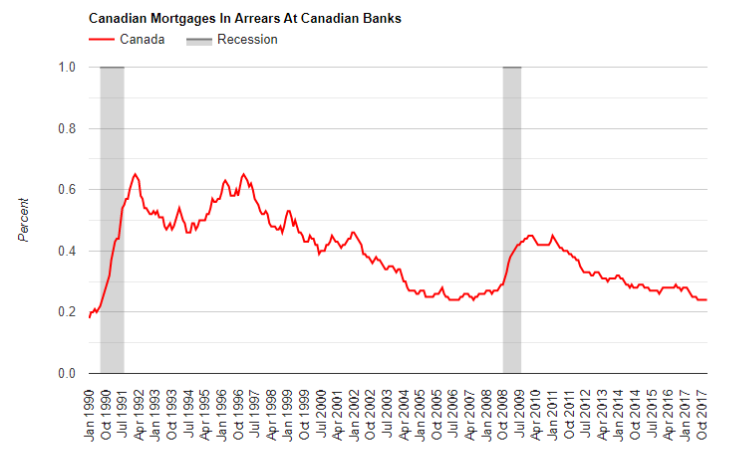

They also use the surplus to cover interim financing costs of their treasury department and finally as an allocation for defaults and loan loss provisions, this is minimal in Canada. Currently, arrears are at about 0.25% and as you can see from the graph below, the worst they have gotten was in the 90’s when they almost hit 0.70%.

The issue is that the Bank of Canada is buying all the mortgages. This means that they are insured against default by the government, so even if the mortgage goes into default, the loss is borne by the Canadian taxpayer. Not the bank.

The banks are acting like a utility here, the water or electricity is the money, the cost being cited is the risk of default, but this isn’t being borne by the banks, so what’s the reason for the increase? Is it because their profits in investment banking and commercial loans will be affected and they want to maintain profitability for their shareholders?

The number to watch will be the increase in their NIM’s (net interest margins) or their overall interest revenue increase for residential mortgages in their next quarterly filing. They will be unable to resist telling their shareholders how smart they were to increase profitability on residential mortgages in the face of rising uncertainty.

Yes, the Canadian Banks are strong, but it’s only because the Canadian consumer is being weakened.