Over the next 3 years, the Canada Mortgage and Housing Corporation (CMHC) could spend an estimated $1.25 billion dollars on the First-Time Home Buyer Incentive (FTHBI). The incentive is intended to increase home ownership affordability for Canadians with incomes at or below $120,000 per year.

Here’s the deal, the CMHC will provide first-time home buyers a 10% down payment on a newly built house, or a 5% downpayment on an existing house. Let’s say the home you’re buying is a new home priced at $400,000, you would receive $40,000 down payment in the form of an interest free loan from the CMHC, and your mortgage would be $340,000 (you would still need to have a minimum of 5% downpayment). Of course, you still also need to comply with the mortgage stress test regulations and make sure that your mortgage is insured. There is also a limit on the combined mortgage amount and incentive at 4 times the buyers’ salary or up to $480,000. The average price for a house in Toronto in August 2018 was just over $780,000, so most properties won’t even qualify for this benefit.

There is also uncertainty regarding the details of the incentive which will be revealed closer to the launch in September. The most critical detail: full payback of the incentive. The first-time home buyer incentive benefit sounds like a steal at first, however it also appears to be an interest free loan which may have to be paid back within a certain timeframe or when the property is sold. It is also unclear if any increase in equity would have to be shared with the CMHC. Moreover, in the case of a loss at the time of sale, it is unknown if the full amount of the incentive would have to be paid back or if the CMHC would share the loss.

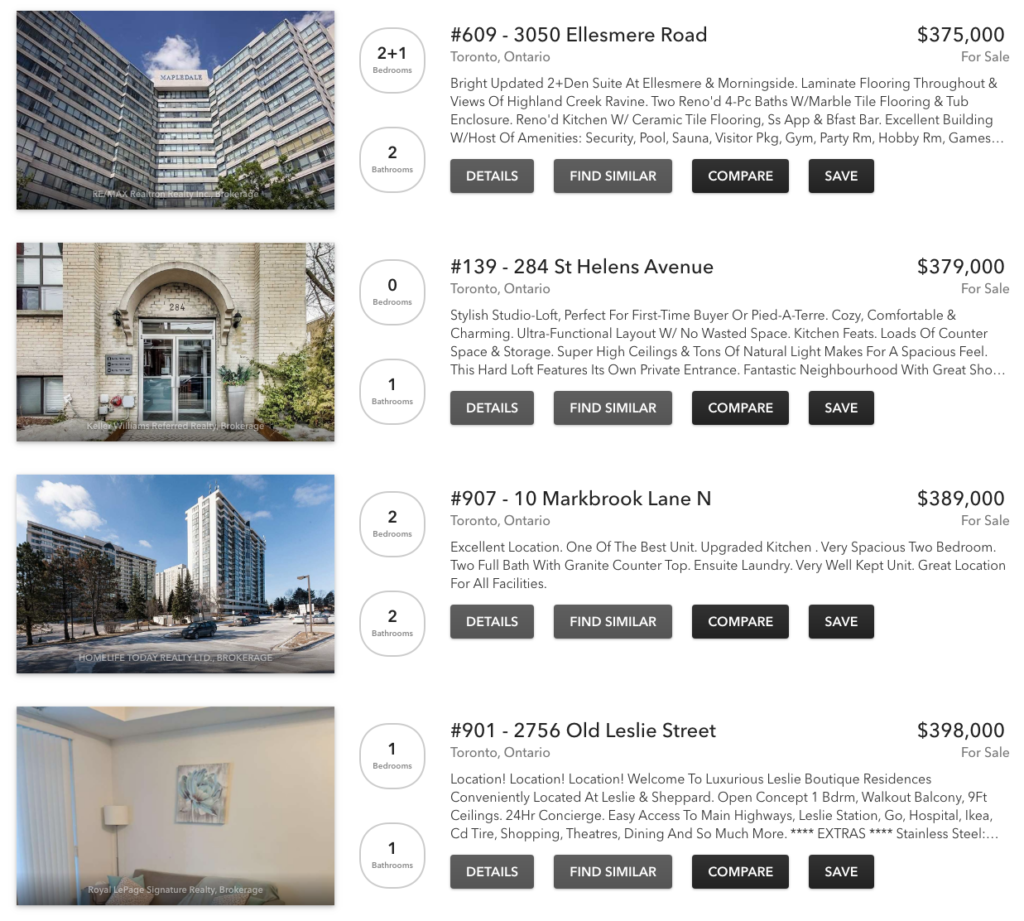

What does a $500,000 home in Toronto really look like?

If first-time buyers can receive an incentive of 5% for an existing home, what are they really getting for a $500,000 property? Can they get a house for this price in Toronto? On the RE/MAX website, there were only four houses listed, and two of them looked like the same house split in half. The other two don’t meet the “under $480,000” qualification standard.

“The incentives in the budget won’t help Torontonians. If you look at the maximum income to qualify for the rebate and the stress test requirements, it means you only qualify for a $500,000 home. Where in Toronto can you find a home for $500,000 these days? You’re no better off with this budget than you are today.”

~Marcus Tzaferis, Cannect CEO

The second part of the announced measures impacts the amount first-time home buyers are allowed to withdraw from their RRSPs to use as down payment. Currently, that’s $25,000. The government is increasing this amount to $35,000 per person or $70,000 per couple. The funds must also be paid back within 15 years, otherwise there are tax implications.

So what does all of this mean? The new budget measures will have minimal impact for first-time home buyers in Toronto. The upper limit of approximately $500,000 is too low to be useful for most homes and condos in this city and the uncertainties regarding payback of the incentive could actually cause potential first-time home buyers to defer the purchase until September. The increase of RRSP withdrawal limit is not as beneficial for the younger generation as they haven’t had enough time to build their savings in order to take full advantage of this incentive benefit. The new measures could prove to be helpful for some Canadians, but are not practical for the majority of first-time home buyers in Toronto.

A solution for first-time Canadian home buyers

Cannect works for Canadians looking to purchase property by giving them the best interest rate on a mortgage. We also provide an alternative to those who have been denied by the banks on a mortgage refinancing or second mortgage option, as well as better borrowing options for self-employed Canadians.

If you’re looking to purchase a new home or refinance an existing mortgage, we’re here to help.