The entire world is now faced with a temporary period of drastically high unemployment, decimated consumer confidence, and mounting consumer debt. COVID 19 is going to wreak havoc on the world’s economy. This is a certainty. What’s equally certain is that things will return back to normal.

Right now, we need confidence, and from what I can tell, we need it in three parts:

Part 1: We need the confidence that if we get sick, there will be a hospital to care for us. This happens when our leaders get started on increasing the number of hospital beds and ventilators available. They must also ensure that our healthcare workers have the protective gear they need to do their jobs.

Part 2: We need the confidence that this evil turd of a virus doesn’t come back again. This will come from the continued efforts to find effective drugs in the short term and eventually a vaccine. The sooner we get a vaccine announced the sooner you will see a massive economic rebound.

Phase 3: We need the confidence that the economic wounds inflicted by this virus don’t scar us permanently. This happens with the proactive steps being taken by the government to protect Canadians from job losses and debt in this period of uncertainty.

Other than being recently glued to the news, I have no epidemiological expertise, so I’ll limit my commentary to the economic realm as it may pertain to the Canadian mortgage market. The benefit of being levelled with an economic crisis like this is that, as long as you can stay positive and focus on the limited time horizon, you will realize that there is a very clearly defined timeline to the hardship. Sure things are bad right now, but just ask quickly as they got bad, they will get better again.

It’s human nature to start planning for the worst, but GDP will eventually re-accelerate against the backdrop of stimulus and low rates. That’s a FACT! It is important to remember that Canada’s economy was strong heading into this virus-induced recessionary period and it will be even stronger after.

Stimulus Offered to Canadian Market as of March 28th, 2020:

Bank of Canada will Buy Debt:

The Bank of Canada will buy close to $150 Billion in uninsured Canadian mortgages. That means liquidity for borrowers. It also means, with some convincing from the Government, we should see mortgage rates fall back in line with their historical premium over bond yields and a more reasonable discount to prime. Have a look at me on BNN this week discussing the matter.

The Prime Rate is Now 2.45%:

**UPDATE: On March 27th, 2020 The BoC dropped the overnight rate by 0.50%. The Overnight Rate in Canada is now 0.25%. They indicated in their press release that this is likely the lowest we will see the overnight rate.

** UPDATE: On March 28th, 2020 The Canadian Banks adopted the entirety of this rate reduction. Prime rate is now 2.45%. With the exception of TD Bank who has decided to keep their 0.15% premium with a prime rate of 2.60%.

The unfortunate issue for Canadians is the rapid increase in mortgage rates, both fixed rates which usually trade about 1.40% above Government of Canada bond yields, and variable rate mortgages which were as low as prime – 1% before COVID. Hopefully the Bank of Canada can convince the Canadian Banks to offer some of the margin in these interest rates to the Canadians who need them most right now. Since these mortgages are now effectively insured by the Canadian Government I see now reason to maintain such egregious spreads.

Reduction in Borrowing Rates:

The Government of Canada is asking banks to reduce the interest rates that Canadians are paying on their credit card balances during this period of economic uncertainty. This could mean lower debt servicing costs at a time when Canadians need it most.

Unemployment Bonus:

Finally, the $2,000 a month being generously provided to anyone unemployed or otherwise affected by the virus should soften the blow to those who can’t earn a wage right now.

Employer Bonus:

Businesses are being offered a 75% wage subsidy in an effort to prevent large scale layoffs.We know that this program will come with some limitations and the Federal Government has yet to release all the details. The previous plan, unveiled a week ago, had the Feds picking up 10% of wages to a maximum of $1,375 per employee and to a maximum of $25,000 per corp.

Small Business Loans:

The Federal Government will be working with the Canadian Banks to offer a maximum of $40,000 to small businesses affected by COVId in the form of a small business loan, of which $10,000 will be forgivable. It would appear that to qualify here business will need to have paid at least $50,000 in total payroll for 2019. These loans will be interest free for the first year. They will be backstopped by the Federal Government and if paid back by 2022, $10,0000 will be forgivable. Again, not all the details of this program have been released yet, but check back with us as we will continue to update details as they are released.

In addition, the Federal Government has authorized The EDC and BDC to extend at least $60 Billion in loans to Canadian companies impacted. These will come in the form of up to $6.25 million in credit from a company’s existing private-sector financial institution with the BDC paying up to $5 million of the loan.

Increasing Funds Available to Lend:

On March 13th, the Office of the Superintendent of Financial Institutions reduced the amount of capital that financial institutions are required to hold in reserve. It is estimated that this will create in excess of $200 Billion in additional lending capacity by the major banks. The next critical step is to ensure that the loans are being provided at market rates. If inflated mortgages rates are any indication our banks might need a little nudge from the Federal Government.

Where are Real Estate Prices Going?

For those of you worried about the value of your home Don’t Be. For the next few months we won’t see much real estate transacting. You might even see a downtick on the average price of a home in Canada. When things start getting back to normal, Canadians will see the effects of generationally low interest rates (one more time) and pent up real estate demand. These two driving factors should catapult real estate prices higher than their pre-COVID peaks.

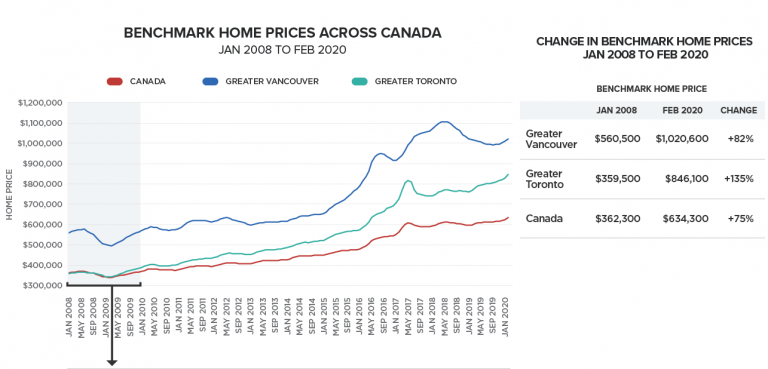

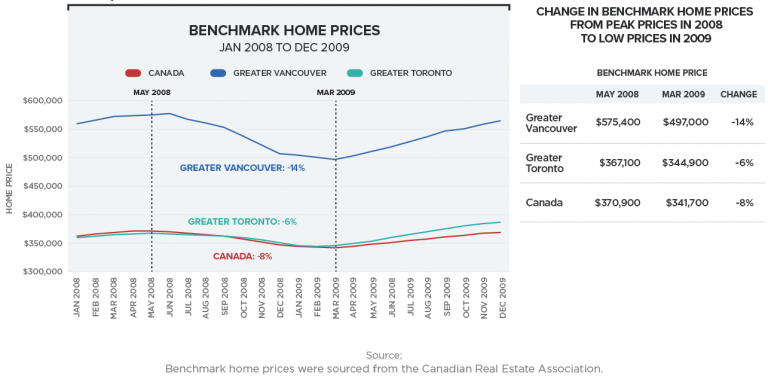

If the previous crisis in 2008 is any indication as to what we are in store for then Canadians should rest assured that property values will be just fine. The GTA saw a 6% drop in housing prices from May 2008 to March 2009, while Canada as a whole saw prices drop by 8%.

I don’t believe we will see much of a drop in housing prices. I also don’t think we can expect to see a repeat of the 135% run up property values enjoyed in the 12 years following January 2008. One thing is certain, you don’t lose 30% in 1 week investing in real estate, that phenomenon is reserved for the stock market.

Use the stimulus that has been offered by the Canadian Government to weather this storm. The folks at Cannect can certainly help you navigate some of the options being offered by the Canadian mortgage lenders. In fact, we wrote about it too, give it a read here.

If you are looking for the best mortgage on the market, or need a second mortgage to bridge you through these turbulent times, we are available to help. It’s business as usual at Cannect!

Thank you all.

Marcus

And thanks to Zoocasa for the great 2008 real estate charts.

To know more details Contact Us Now