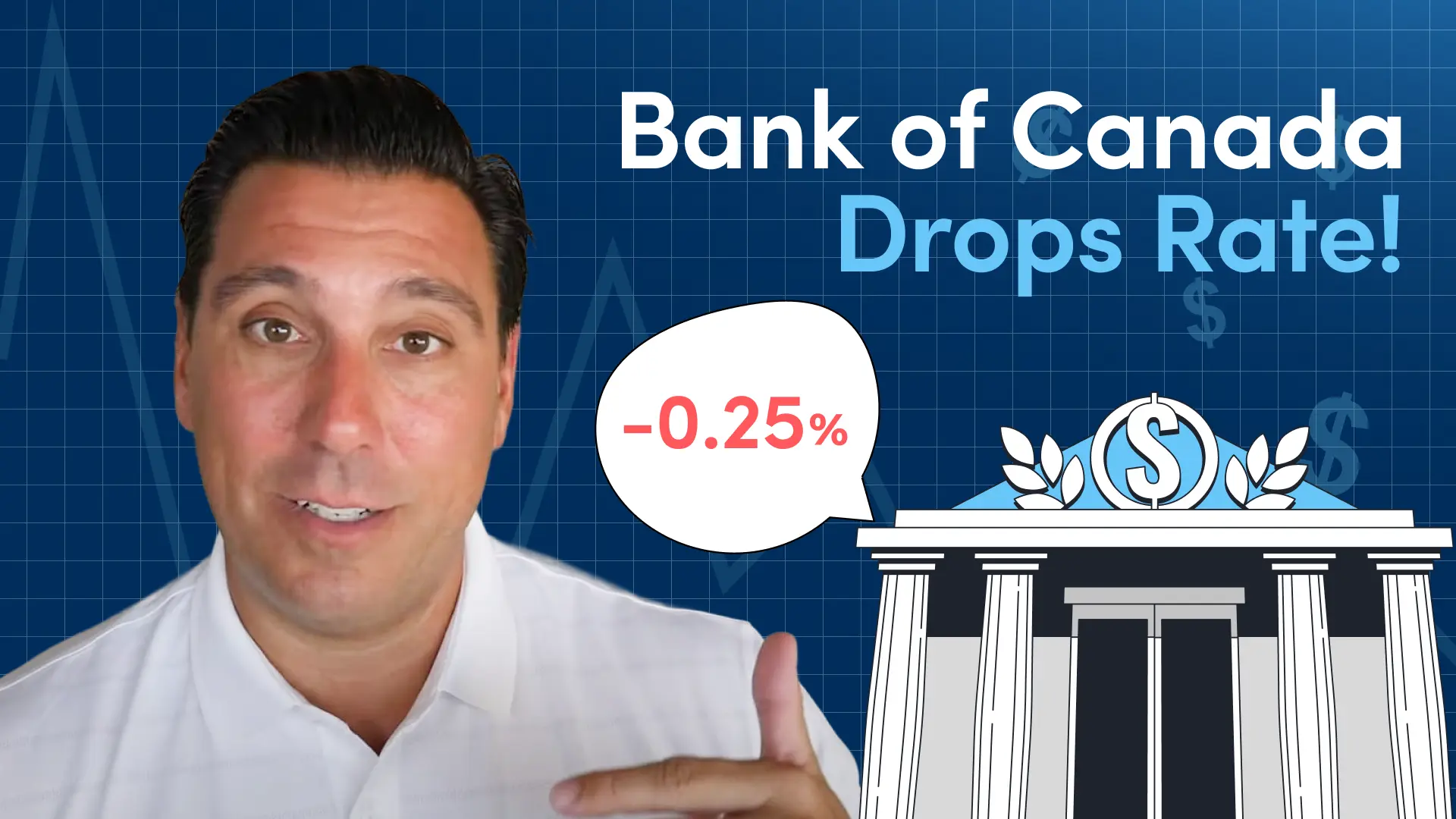

Welcome to the latest episode of Make Money Count! The Bank of Canada has officially cut its overnight rate by 25 basis points, bringing it down to 2.5%. While many homeowners with mortgages are celebrating, this change doesn’t mean the housing market is suddenly going to take off. Instead, it sets the stage for more gradual adjustments and important decisions for anyone considering their mortgage options.

Canada and the U.S.: Moving in Lockstep

Interestingly, the Bank of Canada’s decision came on the same day that the U.S. Federal Reserve also cut rates by 25 basis points. Both countries are responding to similar pressures:

- Tariffs impacting trade and supply chains

- Inflation remains higher than desired.

- Labor market challenges are creating uncertainty.

While U.S. inflation is higher than Canada’s, both economies are showing signs of weakness. This alignment in monetary policy underscores how closely tied our financial systems are.

The State of Canada’s Economy

Beyond inflation, Canada faces bigger structural issues. Business investment has stalled, and confidence is at an all-time low. Productivity is becoming a long-term challenge, while in the short term, recessionary pressures and trade negotiations, including the upcoming CUSMA renegotiations, weigh heavily on the outlook.

As a result, certain sectors, especially the housing market, are already feeling the slowdown.

Why Variable Rate Mortgages Deserve a Second Look

For homeowners and buyers, the biggest takeaway is clear: variable rate mortgages are back in the spotlight. Here’s why:

- Economists are already predicting another 25 basis point cut, likely in October.

- Weak economic conditions point to further rate cuts into 2026.

- Government of Canada bond yields are dropping, pushing fixed rates lower, but variable rates may provide even more flexibility and savings over time.

While attractive fixed rates are available, many borrowers risk “leaving money on the table” if they don’t consider the benefits of going variable in today’s environment.

Fixed vs. Variable: What to Keep in Mind

Fixed mortgage rates are priced off bond yields, which often adjust before Bank of Canada announcements. That’s why fixed rates have already been trending lower. However, as fixed rates drop, penalties for breaking fixed mortgages increase.

If you’re currently locked into a fixed mortgage, it may be worth reviewing:

- The cost of breaking your current mortgage

- Potential savings from switching to a variable rate

- Your long-term financial goals and tolerance for rate changes

At Cannect, we regularly help clients analyze these scenarios to ensure they’re not stuck with an underperforming mortgage.

Will the Rate Cut Revive the Housing Market?

Not immediately. While lower rates may stimulate some activity, one cut won’t reverse the broader economic headwinds. Home prices could continue to soften into 2026, even as borrowing costs come down.

The key is to view these cuts as part of a longer-term trend rather than a quick fix for the housing market.

What This Means for You

If you’re a homeowner or considering buying, now is the time to:

- Review your current mortgage.

- Weigh the benefits of switching to a variable rate.

- Stay informed on upcoming rate announcements and economic shifts.

The market is shifting, and your mortgage strategy should adapt accordingly.

Thinking about making a switch? Talk to Cannect today, we’ll break down the numbers and help you make the most of these changing conditions.