The Canadian economy is at a crossroads. Deloitte recently released a detailed report outlining predictions for 2025 and 2026, with a focus on trade uncertainty, tariffs, and the upcoming renegotiations of the Canada–U.S.–Mexico Agreement (CUSMA).

Deloitte’s Predictions vs. Harsh Realities

The Deloitte report says trade with the U.S. might become stable in the summer of 2026 when KUSMA talks pick up. But Marcus warns that this is just a guess, not a promise. With the U.S. government focused on bringing jobs back to America, Canadian industries like cars, steel, aluminum, and even dairy could face trouble.

Do Canadians really want to rely on uncertain trade talks with an unpredictable U.S. government?

The CUSMA “Mortgage” Analogy

Think of CUSMA like a mortgage that’s up for renewal in 2036. Every year before that, Canada can choose to extend it for another 16 years. But if we start negotiating too early, we might end up with a bad deal—especially if the “lender,” meaning the current U.S. government, is asking for tough terms.

Would you rush to extend your mortgage with a lender giving bad terms, or wait for a better deal?

Trade Uncertainty Is Crushing Confidence

The uncertainty surrounding tariffs is already weighing heavily on Canada:

- Businesses are holding back investments.

- Consumers are spending less.

- Jobs are at risk.

- Confidence in the economy is slipping.

Layer onto that Canada’s own missteps, like immigration policies that boosted short-term growth but now weigh on productivity, and the economic outlook becomes even more fragile.

How long can Canada tread water before these pressures catch up?

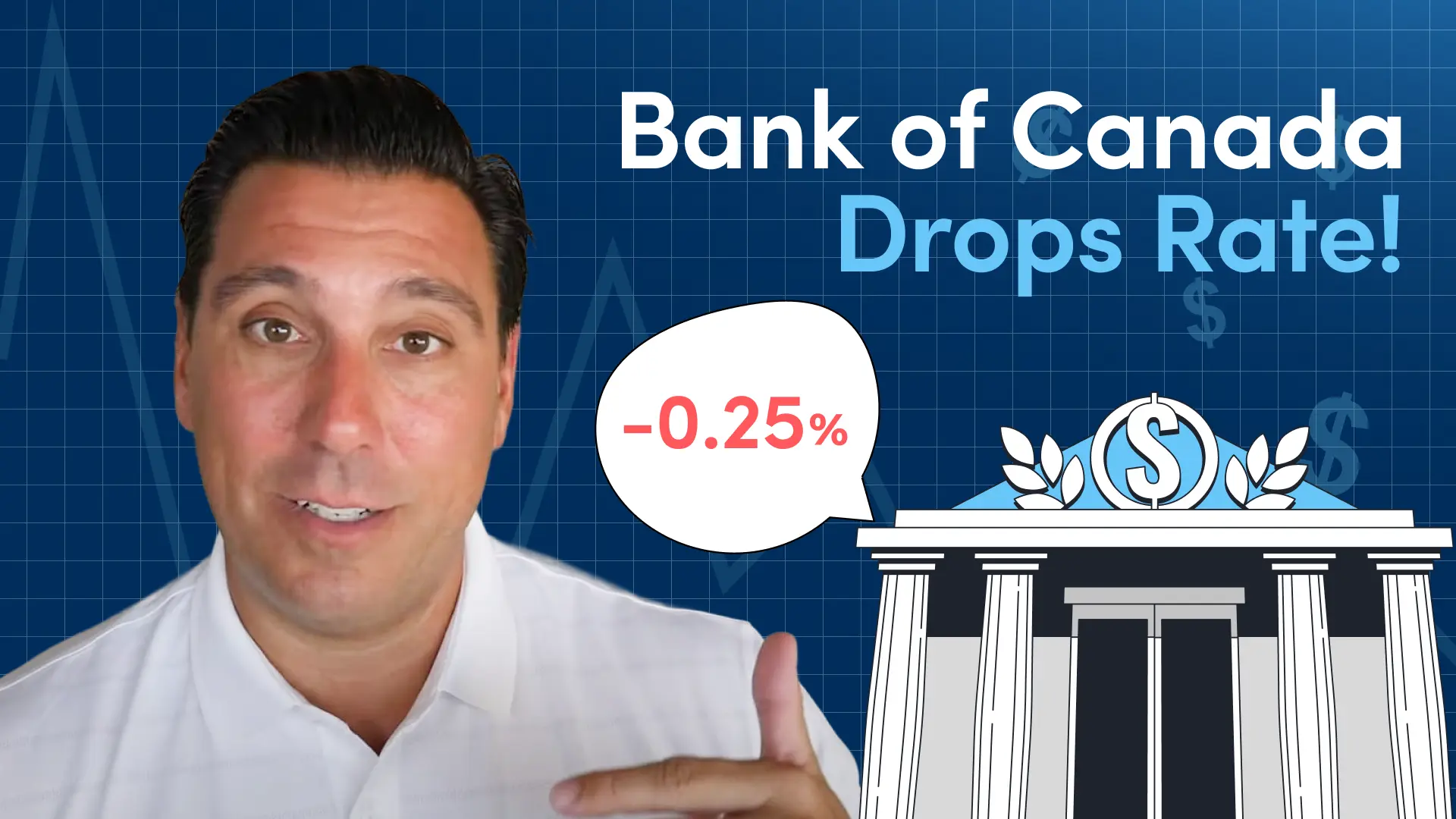

What This Means for Interest Rates

Marcus highlights that bond markets are overestimating stability. With trade uncertainty likely to persist, the Canadian economy may need more monetary stimulus than expected. That means more rate cuts could be on the horizon, even beyond what’s currently priced in.

So, while Deloitte’s report suggests cautious optimism, Marcus believes the downside risks are significantly greater.

Could this mean homeowners are overlooking one of the biggest opportunities in today’s market?

Why Variable Rate Mortgages Still Win

Despite all the noise, one takeaway remains clear: variable-rate mortgages continue to be the smarter choice. Here’s why:

- Rates are likely to fall further as Canada struggles under trade pressure.

- Variable mortgages offer flexibility in uncertain times.

- Homeowners could see “small wins” now when there aren’t many wins elsewhere in the economy

Even if rate cuts don’t arrive in October, Marcus predicts they’ll come faster and harder soon after. Wouldn’t it make sense to position yourself for those gains now instead of locking into a fixed rate?

Final Thoughts

The Canadian economy is being tested by tariffs, trade tensions, and internal policy challenges. While reports like Deloitte’s suggest certainty is just around the corner, Marcus urges caution: certainty with the U.S. is anything but certain.

And for Canadian homeowners, that uncertainty is exactly why variable rate mortgages remain a powerful option.

Curious about whether a variable rate mortgage could work for you? Talk to our team at Cannect today—we’ll walk you through your options and help you make the smartest decision for your future.

Watch our Make Money Count episodes to gain more insights.